CBDC Payment Savings Calculator

Estimated Savings

Traditional Payment Fee:

CBDC Payment Fee:

Total Savings:

Based on 6.25% traditional fee vs 0.5% CBDC fee

The average international transfer fee is 6.25%. With CBDCs, fees can drop below 1%. This calculator shows how much you could save using Central Bank Digital Currencies for cross-border payments.

Central Bank Digital Currencies are not another cryptocurrency like Bitcoin. They’re the digital version of your country’s cash - issued, controlled, and backed by your government’s central bank. Think of them as electronic dollars, euros, or dollars that work just like the paper money in your wallet, but without needing to carry physical bills. Unlike Bitcoin or Ethereum, which are created by networks of strangers, CBDCs are as official as the coins in your pocket. If your government says it’s legal tender, then a CBDC is too.

How CBDCs Are Different From Cryptocurrencies

You’ve probably heard of Bitcoin, Dogecoin, or stablecoins like USDC. They’re all digital, but they’re not the same as a CBDC. Cryptocurrencies are decentralized - no single authority controls them. Their value can swing wildly. Bitcoin jumped 120% in one year, then dropped 40% the next. That’s fine for speculators, but terrible for everyday spending. A CBDC doesn’t work like that. It’s tied one-to-one to your national currency. One digital dollar equals one physical dollar. It won’t suddenly lose half its value overnight. The central bank backs it with the full power of the government. That means if you get paid in CBDC, you know exactly what it’s worth - no guessing, no panic. Also, CBDCs aren’t mined. They’re created and distributed by the central bank, just like printing cash. There’s no blockchain mining rig running 24/7 using electricity the size of a small country. Some CBDCs use blockchain-like tech for security, but most run on private, centralized systems controlled by the bank. That’s not a flaw - it’s the point. You want the government to manage your money, not a decentralized network of anonymous nodes.Why Are Countries Rushing to Launch CBDCs?

Over 130 countries are now working on CBDCs. Why? Because the way we pay is changing fast. In 2024, cash use dropped below 20% in most advanced economies. People use cards, apps, and digital wallets. But those systems aren’t perfect. They rely on banks, payment processors, and intermediaries. Each step adds cost, delay, and risk. A CBDC cuts out the middlemen. Imagine sending money to your cousin in Jamaica. Right now, that costs around 6.25% in fees and takes 1-5 days. With a CBDC, it could cost less than 1% and finish in seconds - even on a weekend. That’s not theory. Nigeria’s eNaira has already cut remittance costs for some users by over 50%. Countries also want more control. When private companies like PayPal or Apple Pay dominate payments, they collect your data, set rules, and sometimes freeze accounts. A CBDC gives the government direct access to the payment system. That means better tax collection, faster stimulus payments during crises, and less reliance on foreign payment networks. In Australia, the central bank tested a wholesale CBDC on Ethereum to automate loan settlements between banks. In China, the digital yuan is used for everything from public transport to government subsidies. Even small nations like the Bahamas have rolled out their own CBDC - the Sand Dollar - to reach remote islands where banks don’t go.How Do CBDCs Actually Work?

There are two main designs: retail and wholesale. Retail CBDCs are for everyone. You download a digital wallet from your central bank’s app, load it with digital cash, and pay for groceries, rent, or coffee. The money is stored on your phone or a smart card. No bank account needed. This is huge for people without access to traditional banking. In Nigeria, over 30% of adults are unbanked. The eNaira gives them a safe, government-backed place to store money. Wholesale CBDCs are for banks and big institutions. They’re used to settle large transactions between financial institutions - like when one bank pays another for a loan. Australia’s proof-of-concept showed this could cut settlement times from days to minutes. That reduces risk and saves billions in operational costs. The technology behind CBDCs varies. Some use distributed ledgers (like blockchain), but most use secure, centralized databases. The key difference from crypto is control. In a CBDC system, the central bank decides who can access the system, what rules apply, and how transactions are verified. Privacy is built in - your transactions aren’t public like Bitcoin’s blockchain. But they’re not completely anonymous either. The central bank can see who sent money to whom, for anti-fraud and tax compliance.

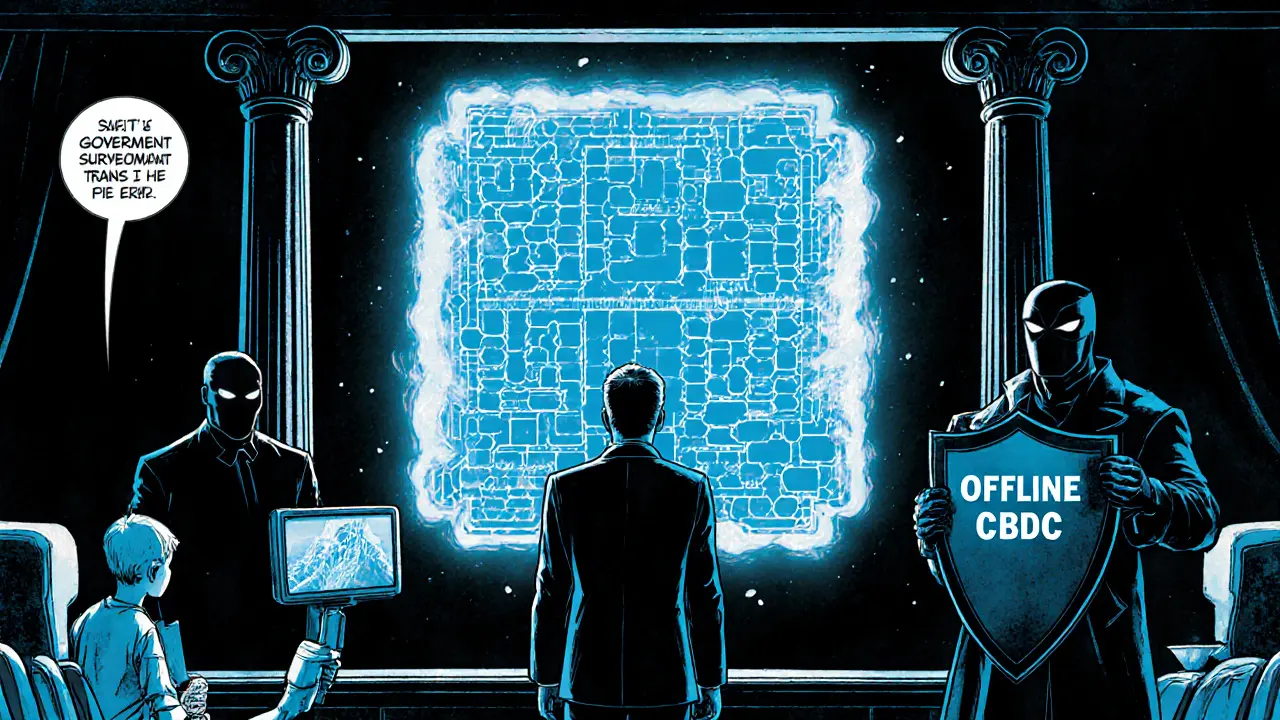

Privacy Concerns and the Risk of Surveillance

This is the biggest debate around CBDCs. Can the government track every purchase you make? The answer is: yes, technically. Unlike cash, which is anonymous, a CBDC leaves a digital trail. If the government wants to, it could see that you bought alcohol at 2 a.m., donated to a political group, or paid for a protest. That’s why privacy advocates warn CBDCs could become tools of control. Some countries are trying to solve this. The European Central Bank’s proposed digital euro includes offline functionality - meaning you could transfer small amounts without the bank knowing. China’s digital yuan offers “controllable anonymity”: small transactions are private, but large ones require identity verification. New Zealand hasn’t launched a CBDC yet, but the Reserve Bank says it’s studying the issue. They’ve said they’d prioritize privacy and financial inclusion. The design will matter. A CBDC that lets you pay anonymously for small amounts, like cash, could win public trust. One that tracks every coffee you buy? That could backfire.What’s the Global Status in 2025?

As of 2025, nine countries have fully launched CBDCs:- Barbados - Sand Dollar (launched 2020)

- Nigeria - eNaira (2021)

- Jamaica - Jamaican Digital Dollar (2022)

- China - Digital Yuan (2020 pilot, nationwide rollout by 2023)

- Russia - Digital Ruble (pilot phase, limited public access)

- India - Digital Rupee (e₹-R, retail pilot ongoing)

- Sweden - e-Krona (testing phase with citizens)

- South Korea - Digital Won (wholesale pilot for banks)

- United Arab Emirates - Project mBridge (multilateral CBDC with China, Hong Kong, Thailand)

Will CBDCs Replace Cash?

No. Not yet. And not necessarily ever. Central banks say CBDCs are meant to complement cash, not kill it. But cash use is falling fast. In Sweden, less than 5% of transactions are in cash. In New Zealand, it’s around 15%. That trend won’t reverse. If cash disappears, CBDCs become the only form of central bank money left. That’s a big deal. Right now, when you hold cash, you’re holding a liability of the central bank. When you hold a bank deposit, you’re holding a liability of a private bank. CBDCs give you direct access to the central bank - no commercial bank in between. That’s powerful. If your bank fails, your CBDC is still safe. Your money isn’t tied to a private company’s balance sheet. It’s backed by the government. That’s why some economists call CBDCs the “ultimate safe asset” for the public.What’s Next for CBDCs?

The next five years will be critical. Countries will start linking their CBDCs for cross-border payments. Imagine sending money from New Zealand to Japan without going through SWIFT or Western Union. That’s already being tested in projects like mBridge, led by the BIS and involving China, Hong Kong, Thailand, and the UAE. Programmable money is another frontier. What if your government gives you a $500 CBDC stimulus payment - but it can only be spent on groceries or solar panels? That’s possible. You could set expiration dates, usage rules, or even auto-deduct taxes. It’s not science fiction. China already uses this for welfare payments. The challenge? Making sure it’s fair. If only big banks can access CBDC infrastructure, small businesses get left out. If the system is too complex, elderly people or rural communities get shut out. The success of CBDCs won’t depend on the tech - it’ll depend on whether people trust it.Final Thoughts

Central Bank Digital Currencies aren’t here to replace Bitcoin. They’re here to replace cash - slowly, carefully, and with purpose. They’re about efficiency, inclusion, and control. For governments, they’re a way to modernize money. For citizens, they’re a new way to hold value - safer than bank deposits, more stable than crypto, and faster than checks. The question isn’t whether CBDCs will happen. They already are. The real question is: how will they be designed? Will they protect your privacy? Will they work for everyone? Or will they become another tool of surveillance and control? The answer will shape the future of money - and your wallet.Are CBDCs the same as Bitcoin?

No. Bitcoin is a decentralized cryptocurrency with no government backing. Its value jumps and falls based on market demand. CBDCs are issued and controlled by your country’s central bank. They’re tied one-to-one to your national currency, so their value stays stable. CBDCs are legal tender; Bitcoin is not.

Can I use a CBDC without a bank account?

Yes. Retail CBDCs are designed to work without a traditional bank account. You can download a digital wallet from your central bank’s app and load it with digital cash using cash, card, or transfer. This is especially important for unbanked populations - like farmers in rural Nigeria or elderly people in remote islands - who don’t have access to banks but still need a safe way to store and spend money.

Will CBDCs track my spending?

Technically, yes - because every digital transaction leaves a record. But how much the government sees depends on the design. Some CBDCs, like China’s digital yuan, allow small anonymous transactions but require ID for larger ones. Others, like the proposed European digital euro, include offline modes so you can pay without the bank knowing. Privacy protections are still being debated - it’s not automatic.

Is my money safer in a CBDC than in my bank?

Yes, in one key way. If your bank goes under, your deposits might be protected up to a limit - but they’re still a liability of the bank. A CBDC is a direct liability of the central bank. That means your money is backed by the full power of the government, not a private company. In a financial crisis, CBDCs are the safest form of money you can hold.

Why haven’t the U.S. or New Zealand launched a CBDC yet?

Both are still researching. The U.S. Federal Reserve says it’s not ready to launch without clear public support and legal clarity. New Zealand’s central bank is studying the risks - especially around privacy and financial stability. They’re cautious because once you launch a CBDC, you can’t easily undo it. They’re watching what happens in Nigeria, China, and the EU before making a move.

Can CBDCs replace international payment systems like SWIFT?

Yes, that’s one of their biggest goals. Right now, sending money across borders takes days and costs up to 6.25%. CBDCs can cut that to seconds and less than 1%. Projects like mBridge - involving China, UAE, Hong Kong, and Thailand - are already testing cross-border CBDC payments. If it works, SWIFT could become obsolete for many transactions.

Do CBDCs use blockchain technology?

Some do, but most don’t need to. Blockchain is often used in crypto for decentralization - but CBDCs are centralized by design. Many central banks use secure, private databases instead. China’s digital yuan uses a hybrid model. Australia’s pilot used Ethereum, but only for bank-to-bank settlements. The tech choice depends on the goal: speed, control, or scalability - not decentralization.

Can I earn interest on my CBDC?

Not currently - but it’s possible. Most CBDCs are designed to be digital cash, not savings. But central banks could add interest in the future. Imagine the central bank paying you 2% interest on your CBDC balance to encourage saving - or charging negative interest to push spending during a recession. That’s called “programmable money,” and it’s one of the most powerful tools CBDCs could give policymakers.

There are 17 Comments

Henry Lu

CBDCs? Please. We already have PayPal and Venmo. This is just the state trying to turn every coffee purchase into a surveillance tick. You think they won’t use this to block people who buy too much weed or donate to the wrong orgs? Wake up. This isn’t progress-it’s digital serfdom.

nikhil .m445

Actually, in India we are already seeing the power of digital rupee. It reduces fraud, cuts transaction cost, and helps small vendors. CBDC is not about control, it is about inclusion. Many poor people have no bank account, but they have phone. This is good thing. :)

Rick Mendoza

CBDCs are just fiat with more steps and zero decentralization. Bitcoin at least lets you own your keys. This? You're trusting the same people who printed trillions during the pandemic to manage your money digitally. Cool. Just cool.

Lori Holton

Oh, so now the government gets to see every single purchase you make? Brilliant. Next they’ll auto-deduct your taxes based on your grocery receipt. And let’s not forget the ‘negative interest’ feature-where they charge you for holding your own money. This isn’t innovation. It’s a dystopian payment system dressed up as convenience.

Bruce Murray

I like that CBDCs could help people without banks. My grandma can’t use apps, but if she could just tap a card and pay for meds without waiting in line at the bank? That’s real progress. I hope they make it simple.

Barbara Kiss

Money has always been a social contract-paper, gold, shells, now bytes. What’s fascinating isn’t the tech, it’s the shift in trust. We used to trust banks. Now we’re being asked to trust algorithms and central authorities. The real question isn’t ‘can we build it?’ It’s ‘should we?’ And more importantly-do we still believe in the people holding the keys?

Aryan Juned

Bro CBDCs are LITERALLY the future 😎 Imagine paying for chai with your phone and the gov sends you a bonus emoji for buying local! 🚀 Also China’s doing it so it’s obviously the right move. Also also I just got paid in digital yuan and it was like… magic? 💸✨

Teresa Duffy

Let’s not forget the rural folks who need this! My cousin in Mississippi can’t get a bank account because she’s ‘high risk.’ A CBDC wallet on her phone? That’s freedom. Let’s make this work for everyone-not just the tech bros.

Sean Pollock

CBDC = Big Brother’s Credit Card. You think the fed won’t freeze your account if you tweet the wrong thing? They already track your amazon buys. Now they’ll know you bought 3 bottles of wine and a protest sign? Yikes. Also i think blockchain is dumb but i still dont trust the gov with my money lol

Carol Wyss

I get why people are scared, but imagine if your kid’s school lunch money was sent directly to the cafeteria via CBDC-no lost checks, no delays. It’s not about control. It’s about making life just a little easier for people who’ve been left behind. Let’s design it right, not just fear it.

Student Teacher

Wait-so if CBDCs are backed by the central bank, does that mean they’re safer than FDIC-insured bank accounts? Because technically, if the bank fails, your deposit is at risk. But a CBDC is direct liability of the government? That’s… actually kind of a big deal. I need to read more.

Ninad Mulay

In India, we’ve seen how UPI changed everything-fast, free, frictionless. CBDC is just the next step. Not about surveillance. About dignity. When your aunt in Bihar can send money to her grandson in Delhi without paying 10% in fees? That’s not control. That’s justice.

Mike Calwell

cbdc? sounds like a scam. why do i need another app? just give me cash. or better yet, barter a chicken.

Jay Davies

It’s worth noting that the UK has been quietly exploring a digital pound since 2021. The Bank of England’s research emphasizes privacy-preserving design, with offline capability and tiered anonymity. The real innovation isn’t the tech-it’s the governance framework. Most public discourse ignores this entirely.

Grace Craig

The notion that CBDCs are somehow ‘neutral’ technology is a dangerous fallacy. Money is power. Power is political. When a central bank can programmatically restrict spending, it transcends monetary policy-it becomes social engineering. This is not a tool for efficiency. It is an instrument of behavioral control, disguised as progress.

Ryan Hansen

Let’s be real-CBDCs aren’t about replacing cash. They’re about replacing the intermediaries. The entire payment ecosystem is built on layers of fees: banks, processors, card networks, foreign exchange brokers. Every time you send money internationally, someone takes a cut. CBDCs cut those layers out. It’s like going from dial-up to fiber optic. The infrastructure changes, but the goal is the same: faster, cheaper, more direct. The privacy debate? Valid. But we’ve had this conversation with credit cards, smartphones, and social media. We adapt. We don’t panic. We demand better design.

Derayne Stegall

CBDCs = 💪🚀 Let’s goooooo! Imagine getting your stimulus check instantly, no delays, no bank holds! And no more paying $30 to Western Union to send money home! This is the future, folks! 🌍💸 #DigitalMoney #NoMoreFees

Write a comment

Your email address will not be published. Required fields are marked *