When you buy Bitcoin or Ethereum, you know the price can swing 10% in a single day. That’s exciting for traders, but useless if you want to pay for groceries, send money overseas, or save without losing half your cash overnight. That’s where stablecoins come in. They’re cryptocurrency that doesn’t act like cryptocurrency-because they’re designed to stay worth exactly $1, €1, or the value of an ounce of gold.

Why Stablecoins Even Exist

Cryptocurrencies like Bitcoin were built to be decentralized and scarce. But scarcity and volatility go hand in hand. If your digital wallet can lose $500 in value while you’re sleeping, it’s not practical for everyday use. Stablecoins fix that. They’re not meant to make you rich overnight. They’re meant to be digital cash-fast, global, and reliable.Think of them as the bridge between traditional money and blockchain tech. You can send a stablecoin across the world in minutes for pennies, no bank approval needed. And unlike bank transfers that only work Monday through Friday, stablecoins run 24/7. That’s why they’re the backbone of DeFi, crypto trading, and cross-border payments.

The Four Types of Stablecoins

Not all stablecoins work the same way. There are four main types, each with different trade-offs between safety, decentralization, and complexity.- Fiat-backed: These are the simplest. For every coin issued, the issuer holds $1 in a bank account-usually in U.S. dollars, euros, or other stable currencies. USDC and EURC are the most trusted examples. They’re audited regularly, and you can redeem them for real money anytime. This is what most people use.

- Crypto-backed: These use other cryptocurrencies (like Ethereum) as collateral. Because crypto prices swing wildly, they’re over-collateralized-meaning you might need $150 worth of Ethereum to issue $100 in stablecoins. MakerDAO’s DAI is the biggest one here. It’s more decentralized than fiat-backed, but riskier if the crypto market crashes hard.

- Algorithmic: These don’t hold any reserves. Instead, they use smart contracts to automatically print or destroy coins based on demand. If the price drops below $1, the system burns coins to reduce supply and push the price back up. Terra’s UST was the most famous example-but it collapsed in 2022 when confidence vanished. Algorithmic stablecoins are high-risk and still experimental.

- Commodity-backed: These are pegged to physical assets like gold or oil. PAX Gold (PAXG) is one example. Each token equals one troy ounce of gold stored in a secure vault. Useful for people who want crypto exposure to gold without buying physical bars.

Fiat-backed stablecoins dominate the market. As of late 2024, over 80% of all stablecoin volume came from USDC and Tether (USDT). They’re simple, trusted, and widely accepted on exchanges and DeFi apps.

How Stablecoins Are Used in the Real World

You might think stablecoins are just for crypto traders. But their real power is in everyday finance.- Trading on crypto exchanges: When you want to exit Bitcoin without cashing out to your bank, you swap it for USDC. That way, you keep your money in the crypto world but avoid price swings.

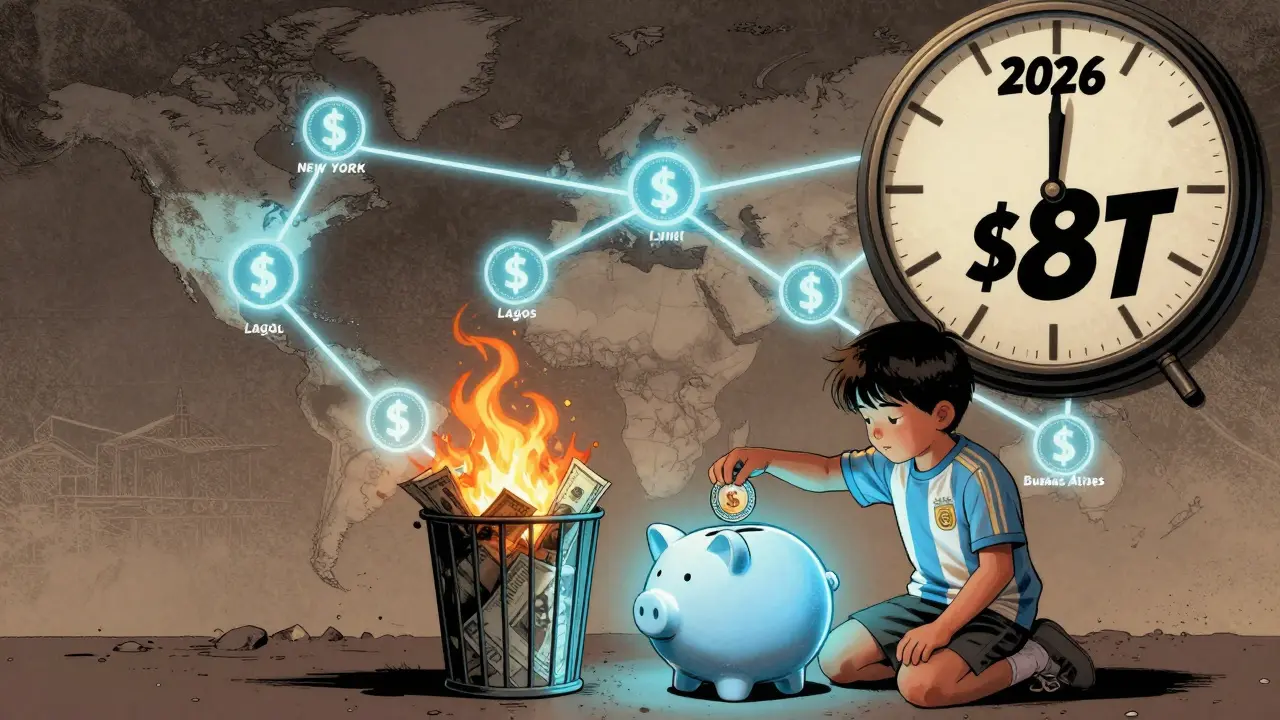

- Send money across borders: Sending $500 from the U.S. to Mexico via Western Union can cost $20 and take days. With a stablecoin, you send it in under 10 minutes for less than $0.50. People in countries with unstable currencies-like Argentina, Nigeria, or Turkey-use stablecoins as their primary savings tool.

- DeFi lending and borrowing: On platforms like Aave or Compound, you can lend your USDC and earn 4-6% interest. That’s higher than most savings accounts, and you don’t need a bank account to do it.

- Payroll and vendor payments: Companies like Shopify and Uber use stablecoins to pay freelancers globally. No currency conversion fees, no delays. Smart contracts can even auto-pay invoices when a delivery is confirmed.

- Store of value: In places where inflation is out of control, people convert their local currency into USDC or DAI. It’s not perfect, but it’s better than watching your savings lose half their value in a year.

The Risks You Can’t Ignore

Stablecoins sound too good to be true-and sometimes, they are.The biggest risk? Trust in the issuer. If the company behind USDC goes bankrupt or freezes your funds, you’re out of luck. That’s why transparency matters. USDC’s reserves are published monthly and audited by Grant Thornton. Tether’s disclosures are less clear, which is why many traders keep only a small portion of their funds in USDT.

Then there’s regulatory risk. In 2025, the U.S. passed the GENIUS Act, which requires all major stablecoins to hold 100% reserves in cash or U.S. Treasury bills. They can’t invest in risky assets. They can’t pay interest. And they must follow strict anti-money laundering rules. This will make stablecoins safer-but also less profitable.

Algorithmic stablecoins? Don’t touch them unless you’re a professional. The UST collapse wiped out over $40 billion in market value in a week. No reserves. No safety net. Just code. And when confidence breaks, the whole system falls.

What’s Next for Stablecoins?

The future of stablecoins isn’t just about being digital dollars. It’s about becoming the new financial infrastructure.Central banks around the world are testing their own digital currencies-CBDCs. China’s digital yuan and the EU’s digital euro will likely compete with private stablecoins. But private stablecoins have one advantage: they’re already here, already used, and already integrated into apps and wallets.

Some companies are now building “yield-bearing” stablecoins that pay interest without breaking regulatory rules. Others are working on privacy-focused versions that protect user data while still meeting AML requirements. And more banks are starting to offer stablecoin wallets directly to customers, blending traditional finance with blockchain.

By 2026, stablecoins will handle over $8 trillion in transactions annually. They’re not going away. They’re becoming essential.

How to Get Started

If you want to try stablecoins, here’s how to do it safely:- Buy USDC or EURC on a reputable exchange like Coinbase, Kraken, or Binance.

- Transfer it to a non-custodial wallet like MetaMask or Trust Wallet. Never leave large amounts on an exchange.

- Use it to trade, send, or earn interest on DeFi platforms like Aave or Curve.

- Always check the issuer’s reserve reports. Look for third-party audits. Avoid anything that doesn’t show proof of backing.

- Don’t put more than you’re willing to lose into algorithmic or crypto-backed stablecoins.

Stablecoins aren’t magic. They don’t solve all the problems of crypto. But they solve the one problem that kept most people away: volatility. For everyday use, global payments, and saving in unstable economies, they’re the closest thing we have to digital cash that actually works.

Are stablecoins really safe?

Fiat-backed stablecoins like USDC and EURC are among the safest digital assets because they’re fully backed by cash or U.S. Treasury bills, and their reserves are publicly audited. But safety depends on the issuer. If the company goes under or freezes your funds, you can lose access. Never assume a stablecoin is 100% risk-free.

Can stablecoins lose their $1 value?

Yes-but only if the system fails. In 2022, Terra’s UST dropped to 70 cents after a bank run. Even USDC briefly dipped to 95 cents during the 2023 Silicon Valley Bank collapse because of temporary reserve concerns. Most stablecoins recover quickly if the issuer has strong backing. But if you see a stablecoin trading below $0.98 for more than a few hours, get out.

Do I need a bank account to use stablecoins?

No. You only need a crypto wallet and access to an exchange that lets you buy stablecoins with a credit card or bank transfer. Many people in countries without reliable banks use stablecoins as their only financial tool. You don’t need credit checks or ID to hold them-though exchanges may require KYC to buy them.

Can I earn interest on stablecoins?

Yes-on DeFi platforms like Aave, Compound, or Yearn. You can earn 4% to 8% APY by lending your USDC or DAI. But these platforms are not FDIC-insured. If the smart contract has a bug or the platform gets hacked, you could lose your money. Only use well-audited protocols and never invest more than you can afford to lose.

Are stablecoins better than Bitcoin for daily use?

Absolutely. Bitcoin’s price changes too much to be practical for buying coffee or paying rent. A stablecoin holds its value, so you know exactly how much you’re spending. It also settles faster and costs less than Bitcoin transactions. For daily use, stablecoins are the clear winner.

What’s the difference between USDC and Tether (USDT)?

Both are dollar-backed stablecoins, but USDC is issued by Circle and is fully transparent-its reserves are published monthly and audited by a major firm. Tether is issued by Bitfinex and has faced criticism for lacking full transparency. USDT is more widely used, but USDC is preferred by institutions and regulated platforms because of its openness.

There are 21 Comments

steven sun

Catherine Hays

Chidimma Catherine

Taylor Mills

Arielle Hernandez

Ryan Depew

Jessica Boling

Tammy Goodwin

Brenda Platt

Harshal Parmar

Melissa Contreras López

Mike Stay

Barbara Rousseau-Osborn

Darrell Cole

HARSHA NAVALKAR

Adam Lewkovitz

Jen Allanson

Clark Dilworth

Mathew Finch

Adam Fularz

Nathan Drake

Write a comment

Your email address will not be published. Required fields are marked *