Nigeria Crypto Market Impact Calculator

Estimated Impact Summary

Total Annual P2P Volume:

Informal Economy Contribution:

Scam Reduction Impact:

Community Trust Level:

Note: This calculator uses data from Nigeria's 2021-2023 crypto ban period. Values are estimates based on reported statistics.

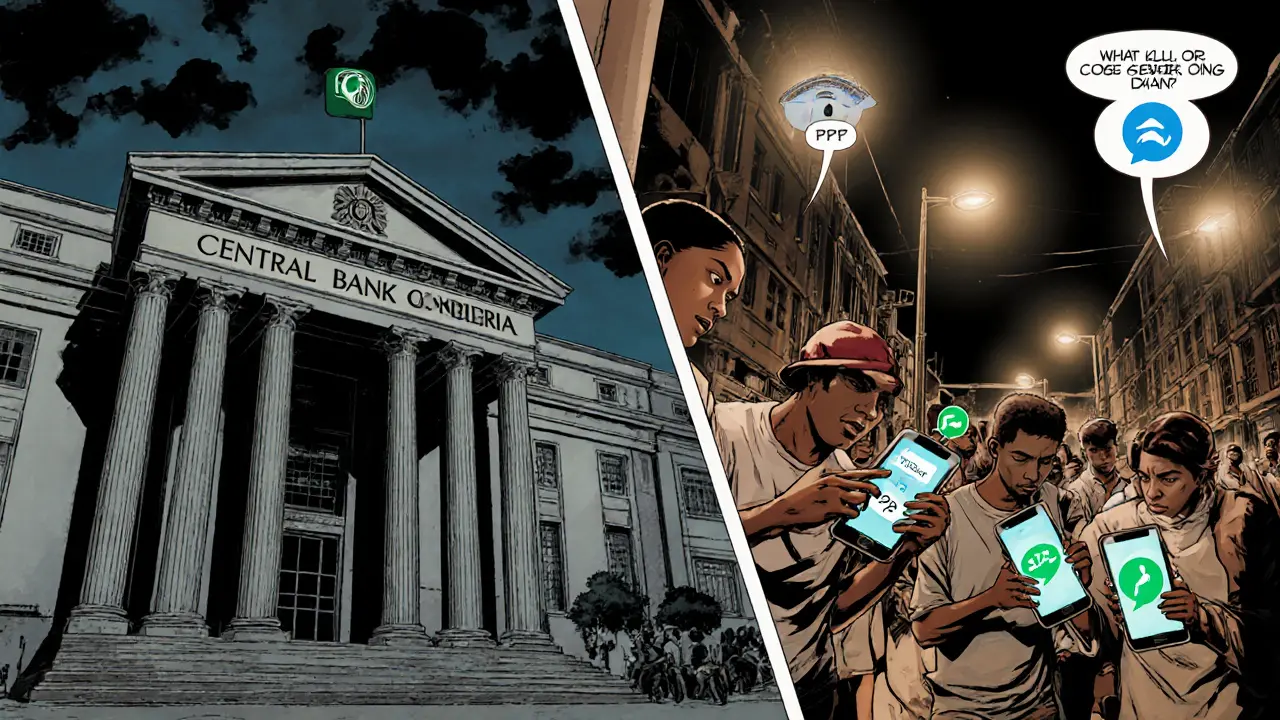

When the Central Bank of Nigeria (CBN) shut its doors to crypto in February 2021, most expected the market to wither. Instead, a hidden network exploded, driven by peer‑to‑peer traders, WhatsApp groups and a do‑it‑yourself spirit that turned the ban into a catalyst.

Key Takeaways

- The ban pushed crypto activity into an underground economy worth billions, with P2P platforms processing up to $150million a month.

- WhatsApp and Telegram became the main trust‑building tools, while Binance P2P emerged as the dominant exchange.

- Despite rapid growth, fraud remained high; community‑run blacklists and test‑trade protocols cut scams by roughly one‑third.

- The underground market accounted for about 3% of Nigeria’s informal economy and positioned the country as the world’s second‑largest crypto adopter.

- Regulators are now trying to integrate the lessons learned, but new restrictions hint that a hybrid formal‑informal ecosystem will persist.

Below, we unpack how this shadow market formed, how everyday Nigerians navigated it, and what the legacy means for the next wave of regulation.

What sparked the underground surge?

Underground crypto economy in Nigeria is a network of informal, peer‑to‑peer crypto trades that operates outside regulated financial institutions. The catalyst was the Nigeria crypto ban announced on 5February2021, which instructed banks to close any accounts linked to crypto activity. While individuals could still own digital assets, the ban cut off the most convenient fiat‑to‑crypto gateway.

Faced with a sudden liquidity crunch, traders turned to online messaging apps. A 2022 Breet.io survey showed 78% used WhatsApp groups to verify counterparties, and 63% relied on Telegram channels for price discovery. The result was a parallel financial layer that mimicked traditional exchanges-only faster, cheaper and completely unregulated.

How P2P platforms became the backbone

Binance P2P quickly rose to prominence. By Q32022 it boasted over 1.2million Nigerian users and handled roughly $150million in monthly naira‑denominated trades. Its escrow system, powered by multi‑signature smart contracts, gave users a sense of security without needing a bank.

Other platforms like Paxful and local innovators such as Quidax and Bundle also contributed. Paxful data reported that Nigerians accounted for 32% of its global escrow transactions during the ban, underscoring the country’s outsized role.

Typical trade flow looked like this:

- Trader A posts a sell order on Binance P2P, specifying price and payment method (often a bank transfer limited to ₦500,000).

- Trader B locks the crypto in escrow and sends a small test payment (e.g., ₦5,000) to confirm the bank details.

- After the test clears, the full amount is transferred, and the escrow releases the crypto.

This “test‑trade” protocol, popularized by community groups, cut scam rates by about 37% according to CryptoNaija’s 2022 report.

Risk management in a law‑less environment

Without formal KYC/AML oversight, fraud surged. Monierate’s 2022 study found 42% of traders had experienced at least one scam. To combat this, users built crowd‑sourced blacklists shared across WhatsApp groups of 50,000+ members. These lists flagged repeat offenders, reducing repeat victimization.

Dispute resolution also evolved. The Telegram‑based “Naija Crypto Arbitration Group” settled roughly 1,200 cases per month by late 2022, offering refunds or escrow reversals when a party disappeared.

Nevertheless, the cost was high: 67% of users who received crypto payments through informal channels later faced frozen bank accounts, forcing many to switch to mobile‑money or airtime exchanges.

Economic impact: volumes, demographics, and adoption

Chainalysis estimated that Nigerian crypto transaction volume hit $56.7billion between July2021 and June2022-about 1.2% of all global crypto activity despite Nigeria representing just 0.1% of global GDP. In 2022 alone, the underground market moved $18.3billion, equating to roughly 3% of the country’s informal economy.

Who were the players? A Creditcoin.org survey showed 68% of traders were aged 18‑35, with students (41%) and small‑business owners (29%) leading the charge. The average new user spent 2‑3weeks learning safe P2P practices before feeling comfortable.

Success stories surfaced: Reddit user “LagosTrader87” turned a ₦5,000 seed capital into a ₦2.3million portfolio within 18months, funding his university education. Conversely, “AbujaInvestor” lost ₦380,000 to a disappearing seller, illustrating the thin line between profit and loss in an unregulated market.

Comparison: Underground vs. Formal Crypto Trading

| Aspect | Underground (P2P) | Formal (Bank‑linked) |

|---|---|---|

| Regulatory oversight | None; community‑driven trust mechanisms | CBN and banking regulations, KYC/AML |

| Monthly transaction volume | ~$150million (Binance P2P) | ~$30million (licensed exchanges) |

| Typical transaction size | Under ₦500,000 / $600 | Above ₦1million / $1,200 |

| Fraud risk | High (42% reported scams) | Lower, but still present |

| Liquidity | Strong for BTC/USDT via P2P | Limited to listed pairs |

| User trust | 89% trust P2P over banks | 70% trust banks |

Legacy and the road ahead

When the ban lifted in December2023, the CBN issued new guidelines that still barred banks from holding or transacting in virtual currencies. The February2024 crackdown on Binance P2P signaled regulator fatigue with peer‑to‑peer models. Yet the cultural shift persisted-89% of Nigerians now view crypto as a legitimate financial tool, according to a Techpoint Africa survey.

Future policy, like the March2025 Investments and Securities Act, aims to classify digital assets as securities, while a 2026 tax on crypto profits may push some activity back underground. Experts such as Dr. Yemi Babarinsa argue that Nigeria’s experience proves “regulatory bans often accelerate adoption, creating hybrid ecosystems that force regulators to adapt.”

In practice, many traders now maintain accounts across multiple platforms-82% of experienced users juggle at least three exchanges-to hedge against sudden closures. Community education continues via YouTube channels like “Crypto With Tolu,” which amassed 247000 subscribers by 2023, offering tutorials on secure P2P trading, escrow usage, and dispute arbitration.

Frequently Asked Questions

Why did the underground crypto market grow faster than the formal one?

The ban cut off bank‑based fiat gateways, forcing users to seek alternatives. Peer‑to‑peer platforms offered immediate liquidity, low fees, and a trust network built on WhatsApp and Telegram, which scaled faster than the limited licensed exchanges.

Is trading crypto still illegal in Nigeria?

Individuals can own and trade crypto, but banks cannot facilitate those transactions. The CBN allows licensed exchanges to operate with strict compliance, while P2P trading remains in a legal gray area.

How can I protect myself from scams on P2P platforms?

Use escrow services, start with a small test payment, verify the counter‑party’s reputation on community blacklists, and consider arbitration groups for dispute resolution.

What was the total crypto transaction volume during the ban?

Chainalysis estimates $56.7billion between July2021 and June2022, with the underground segment handling roughly $18.3billion in 2022 alone.

Will future regulations push crypto back underground?

Potentially. New taxes and tighter licensing could make formal channels costlier, encouraging users to revert to trusted P2P networks unless regulators provide a seamless, low‑cost alternative.

In short, the ban didn’t kill crypto in Nigeria-it forged a resilient, community‑powered market that continues to shape policy and innovation. Understanding how that underground ecosystem works is essential for anyone looking to navigate or regulate crypto in Africa’s biggest economy.

There are 16 Comments

Annie McCullough

Crypto P2P dynamics are just a classic case of regulatory arbitrage 🤓

Carol Fisher

It's outrageous that any government tries to crush financial freedom – the Nigerian people showed the world how to hustle! 🚀💪

Hanna Regehr

The underground market basically built its own escrow system using community trust.

WhatsApp groups acted like informal KYC, checking each other's reputation.

That grassroots verification cut scams dramatically without any regulator involvement.

It also kept transaction fees low, which is why so many small traders jumped in.

Overall, the model proved that decentralized trust can thrive under pressure.

Ben Parker

Yo you think that's all? Imagine being forced to use cash only – nightmare 😂

Daron Stenvold

When we examine the sociopolitical undercurrents, the Nigerian response reads like a modern ode to resilience.

Regulatory suppression, rather than extinguishing demand, illuminates the primal human drive for financial autonomy.

The community‑driven escrow mechanisms emerged not as a stop‑gap but as a sophisticated, emergent institutional framework.

Such organic governance, while lacking formal oversight, nonetheless instituted reputational penalties that rivaled traditional banking sanctions.

The drama of a state versus the ingenuity of the populace underscores a timeless narrative of power and ingenuity.

In short, the episode affirms that top‑down prohibitions often catalyze bottom‑up innovation.

hrishchika Kumar

From a cultural perspective, the Nigerian youth leveraged familiar social tools – WhatsApp and Telegram – to forge a new economic lingua franca.

It’s a beautiful example of how technology blends with local customs, turning everyday chat groups into trusted trading floors.

The colorful memes and shared dialects created a sense of belonging that banks could never replicate.

This cultural fabric is what kept the underground market alive even when authorities tightened the screws.

Nina Hall

Seeing such ingenuity gives me hope for other emerging markets.

When people are motivated, they’ll find a way around any obstacle.

Keep the positive vibes flowing, Nigeria!

Emily Kondrk

Don't forget the hidden strings – every time you think the system's safe, a shadow group is pulling the levers.

The ban was just a smokescreen, and those who whisper in dark Telegram channels know more than we’re told.

Stay awake, stay skeptical – the crypto underworld is a rabbit hole of secrets.

Laura Myers

Wow, the sheer scale of that underground empire blows my mind! 🎭

Anjali Govind

It’s fascinating how quickly people adapt – the data shows a steep learning curve in just a few weeks.

Anyone else notice the pattern of rapid skill acquisition?

Sanjay Lago

bro i think its awesome how they turned whatsapp into a crypto market lol

i used to think crypto was only for geeks but now i see everyone can hustle

Ted Lucas

Leveraging P2P escrow is basically the MVP of decentralized finance in practice. 🚀

The test‑trade protocol acts as a low‑friction KYC, reducing fraud risk without heavy compliance overhead.

Moreover, the network effect multiplied liquidity across Binance, Paxful, and local solutions.

This organic scaling showcases the power of network‑driven liquidity provision.

Bottom line: the underground model is a live case study for DeFi architects.

Manas Patil

From a cultural lens, the Nigerian crypto surge mirrors historical market adaptations where informal trade routes filled gaps left by colonial banking systems.

It's a modern reenactment of how societies create parallel economies when formal channels become exclusionary.

The colors, slang, and community rituals around crypto echo those of traditional market bazaars.

This cultural continuity makes the crypto phenomenon more than just a tech story – it's a social evolution.

mark noopa

Consider, for a moment, the ontological implications of a state‑mandated prohibition colliding with an emergent, decentralized financial ecosystem. The paradox lies not merely in the superficial evasion of regulation, but in the profound reconfiguration of trust vectors within a society historically bound by hierarchical institutions. When banks withdraw their fiat conduits, the void is not a vacuum; it is an invitation for collective agency to co‑opt existing digital scaffolds-WhatsApp, Telegram, and the very code of Binance's P2P escrow-recasting them as makeshift fiduciary custodians. This transformation is emblematic of a broader dialectic where power attempts to enforce order, yet order organically migrates to the periphery, reshaping itself into a resilient, adaptive lattice. The data points-$150 million monthly volume, a 37 % reduction in scams via community‑driven test‑trade protocols, and a 3 % contribution to the informal economy-are not merely statistics; they are signifiers of a societal shift toward decentralized risk management. Moreover, the psychological substrate of the participants-young entrepreneurs, students, small business owners-reveals a generational willingness to embed themselves within a network that rewards reputation over regulatory compliance. This reputational economy, while lacking formal KYC/AML safeguards, paradoxically enforces its own discipline through crowd‑sourced blacklists and arbitration groups that resolve disputes with a quasi‑judicial efficiency. In the grand tapestry of financial history, one might argue that this is the latest iteration of an age‑old pattern: when official channels close, the market mutates, leveraging technology to preserve liquidity and trust. The Nigerian example, therefore, is not an anomaly but a case study in the inevitable emergence of parallel financial strata when governance attempts to stifle innovation. As regulators recalibrate-introducing hybrid frameworks that recognize both formal and informal actors-the future may well be a symbiosis rather than a binary conflict, wherein the lessons of the underground inform more inclusive, resilient policy. Ultimately, the narrative underscores a timeless truth: prohibition rarely extinguishes demand; it merely reshapes its vessel.

Rama Julianto

Alright, let’s cut the fluff – this underground scene is a goldmine for anyone daring enough to dive in. The community‑run blacklists are brutally effective; if you mess up once, you’re out. Use the test‑trade protocol every single time, no excuses. Remember, the stakes are high, but the rewards are massive when you play it right. Stop whining and start learning the ropes.

Helen Fitzgerald

Great discussion, everyone – keep sharing knowledge and stay safe!

Write a comment

Your email address will not be published. Required fields are marked *