For years, the idea of putting your digital assets in a traditional bank felt like a contradiction. Banks were seen as slow, rigid institutions wary of technology, while crypto was the wild west of finance. But if you look at Switzerland today, that narrative has completely flipped. Swiss banks aren't just tolerating cryptocurrency; they are leading the charge in regulated custody and services. By mid-2026, institutions like Sygnum Bank and Amina Bank have become global benchmarks for how to handle digital assets safely.

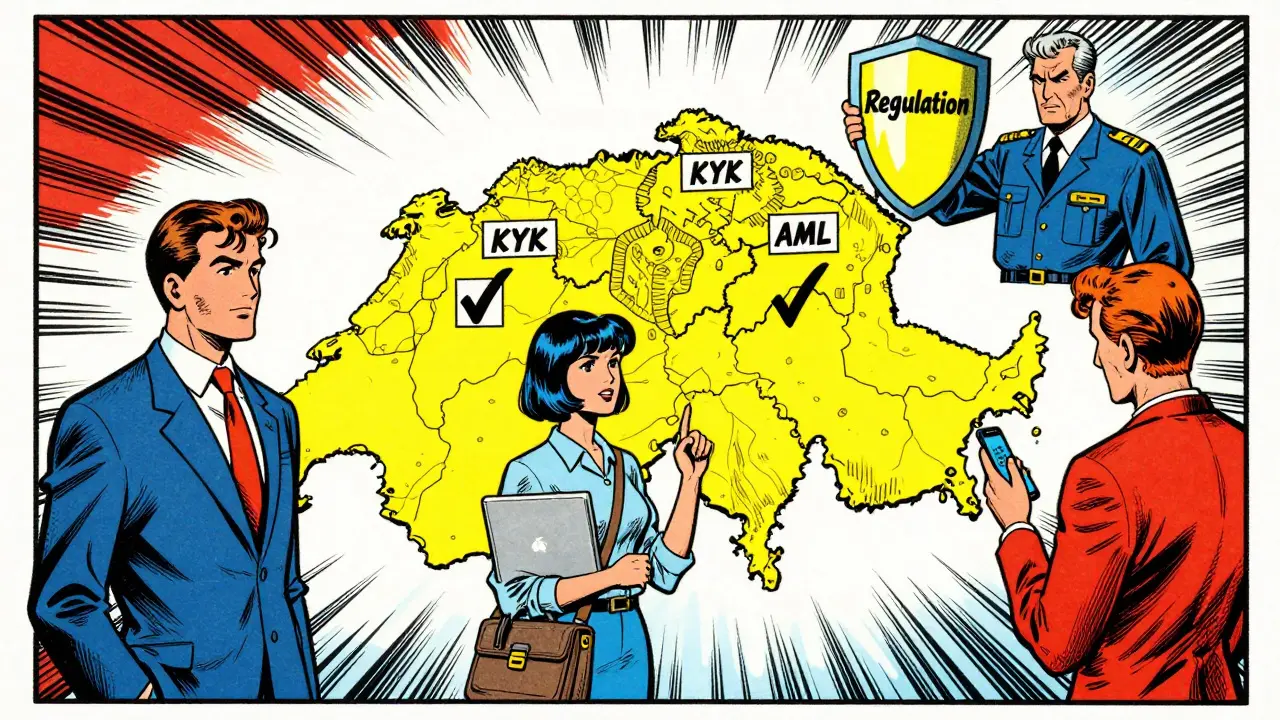

But here is the catch: this isn't a free-for-all. The "restrictions" mentioned in your search aren't bugs in the system-they are the feature. Switzerland’s approach relies on strict regulatory frameworks that many other countries are still trying to figure out. Understanding these rules is crucial if you want to use these services. You don't get access by hiding behind anonymity; you get it by meeting rigorous compliance standards. This article breaks down what Swiss banks actually offer, who can use them, and why their security model is considered the gold standard.

The Regulatory Foundation: Why Switzerland Leads

To understand why Swiss banks dominate crypto custody, you have to look at their legal strategy. Unlike jurisdictions that tried to create entirely new laws from scratch-often resulting in confusion or bans-Switzerland took a technology-neutral approach over five years ago. They applied existing financial market legislation to digital assets. This means a token is treated similarly to a share or a bond, depending on its function, under the supervision of the Financial Market Supervisory Authority (FINMA).

This early move created a stable environment. When the United States issued joint regulatory statements in 2025 emphasizing that banks must only offer crypto safekeeping that is "safe and sound," Switzerland had already been operating under those principles for years. This head start allowed Swiss banks to build mature, compliant infrastructures while others were still debating basics. For an investor, this stability translates to lower counterparty risk. You know the bank won't be shut down overnight because the rules are clear.

The restrictions here are primarily about identity and source of funds. Swiss banks enforce enhanced Know Your Customer (KYC) and Anti-Money Laundering (AML) measures. If you are looking for anonymous trading, a Swiss bank is not the place. If you are an individual or institution wanting secure, legal exposure to crypto, it is one of the best places on earth.

Key Players in Swiss Crypto Banking

Not all Swiss banks offer the same crypto services. While some traditional giants remain cautious, specialized institutions have emerged as leaders. Here are the primary entities shaping the landscape:

- Sygnum Bank: One of the first fully licensed banks in Switzerland dedicated to digital assets. They focus heavily on institutional clients but also serve high-net-worth individuals. Their platform allows for custody, trading, and lending of various tokens.

- Amina Bank: Known for integrating crypto into everyday banking. They offer accounts for both individuals and corporations, including specialized packages for startups. Amina was notably the first regulated bank globally to support the Sui blockchain's native token.

- Bitcoin Suisse: Originally a trading firm, they expanded into banking and custody. Their "Bitcoin Suisse Vault" is a prominent institutional solution known for its physical and cryptographic security layers.

- Swissquote: A well-established online broker that added comprehensive crypto trading and custody options, appealing to retail investors who want a familiar interface.

Each of these institutions operates under the same FINMA umbrella, but their service portfolios differ. Sygnum might be better for complex institutional lending structures, while Amina could be more attractive for a tech startup needing payroll in stablecoins. Choosing the right bank depends on whether you prioritize advanced API integration, user-friendly mobile apps, or specific asset coverage.

Custody Solutions: How Your Assets Are Protected

Custody is the core service here. It’s not just about holding keys; it’s about protecting them against theft, loss, and human error. Swiss banks employ multi-layered security models that go beyond simple password protection.

Take Bitcoin Suisse Vault as an example. Their institutional custody solution combines cryptographic security with physical safeguards. Private keys never leave Switzerland, reducing jurisdictional risk. They use redundant backup systems to protect against cyberattacks, hardware failures, and even electromagnetic pulse interference. This level of paranoia is necessary when managing millions in digital value.

Most Swiss crypto banks use a multi-signature (multi-sig) setup. This means no single employee can move your funds. Transactions require approval from multiple authorized parties, often using hardware security modules (HSMs) stored in geographically dispersed locations. Some banks also offer cold storage solutions where assets are kept offline, accessible only through strict procedural controls.

| Institution | Primary Focus | Custory Features | Key Differentiator |

|---|---|---|---|

| Sygnum Bank | Institutional & HNW | Multi-sig, HSM-backed | Broad token support, lending services |

| Amina Bank | Retail & Corporate | Integrated banking app | Stablecoin rewards, startup packages |

| Bitcoin Suisse | Institutional | Physical + Crypto vault | Proprietary vault, low-latency APIs |

| Swissquote | Retail Investors | Standardized custody | User-friendly interface, wide asset list |

Service Offerings Beyond Storage

Custody is just the entry point. Swiss banks offer a suite of services that integrate crypto with traditional finance. These include:

- Trading: Access to spot markets for major cryptocurrencies. Some banks offer direct exchange rates without hidden spreads, though fees vary.

- Lending: Institutions like Sygnum allow clients to borrow against their crypto holdings. This provides liquidity without triggering taxable events from selling assets.

- Staking: Many banks now offer staking services for proof-of-stake blockchains. For example, Bitcoin Suisse supports staking for Ethereum (ETH), Solana (SOL), Cardano (ADA), and Polkadot (DOT). This lets you earn yield on your idle assets while maintaining regulatory compliance.

- Governance Participation: Advanced clients can participate in network votes for supported assets. This is crucial for decentralized finance (DeFi) projects where community decisions shape the future of the protocol.

In August 2025, Sygnum and Amina expanded their offerings to include the SUI token. This move wasn't just technical; it signaled strong institutional demand. Trading volume for SUI doubled immediately after the announcement, rising to 36.45 million tokens compared to the daily average. The price stabilized around $3.82, showing that regulated access drives serious capital into emerging ecosystems.

Restrictions and Eligibility: Who Can Use These Services?

This is where the "restrictions" part of your query becomes critical. Swiss crypto banks are not open to everyone, and their terms are stricter than offshore exchanges.

Residency and Identity: While some services are available internationally, full banking relationships often require residency in supported jurisdictions or significant wealth verification. You will need to provide government-issued ID, proof of address, and detailed information about your source of wealth. Non-resident aliens may face additional scrutiny under US FATCA regulations if they interact with certain platforms.

Asset Types: Not every token is accepted. Banks generally stick to established cryptocurrencies with clear utility and regulatory status. Highly speculative memecoins or unregistered securities tokens are usually excluded. The bank acts as a gatekeeper, ensuring that the assets they hold meet legal standards.

Minimum Balances: Institutional services often have high minimum deposit requirements, sometimes starting at €100,000 or more. Retail-oriented banks like Amina or Swissquote may have lower thresholds, but premium features still come with costs.

Geopolitical Sanctions: Swiss banks adhere strictly to international sanctions lists. If you are located in a sanctioned country, you will not be able to open an account. This is non-negotiable due to FINMA's enforcement powers.

Security and Compliance Infrastructure

Trust in a bank comes from its ability to protect data and assets. Swiss crypto banks invest heavily in cybersecurity infrastructure. They comply with the General Data Protection Regulation (GDPR) for data privacy, ensuring your personal information is handled with care. However, crypto adds a layer of complexity: private key management.

Banks use predictive threat assessment tools to detect unusual activity before it becomes a breach. They conduct regular penetration testing and audit their smart contracts if they interact directly with DeFi protocols. In case of a cyber incident, Swiss banks typically carry insurance policies that cover customer losses, though limits apply. Always check the specific coverage details in the terms of service.

Furthermore, the regulatory framework requires banks to maintain sufficient capital reserves. This means they cannot lend out all your crypto or take excessive risks with your collateral. This prudential regulation is a key difference between a bank and a centralized exchange like FTX, which collapsed due to poor risk management and lack of oversight.

Future Outlook for Swiss Crypto Banking

By 2026, the trend is clear: integration. Swiss banks are moving towards omnichannel experiences where crypto and fiat currencies coexist seamlessly. You can pay bills with stablecoins, receive salary in Bitcoin, and hedge risk with traditional stocks-all within one dashboard. Data analytics are being used to offer personalized financial products, making crypto accessible to a broader audience while maintaining safety.

The sector is also diversifying revenue streams to mitigate volatility. Partnerships with fintech companies and cross-border collaborations are expanding. As global regulators catch up, Switzerland’s early lead ensures it remains a preferred hub for institutional crypto adoption. For investors, this means greater stability, clearer legal recourse, and professional-grade tools for managing digital wealth.

Can I open a Swiss crypto bank account if I live outside Switzerland?

Yes, many Swiss crypto banks accept international clients, but eligibility depends on your country of residence. Banks must comply with local laws and international sanctions. Residents of sanctioned countries cannot open accounts. Additionally, non-residents may face higher minimum balance requirements or limited service features compared to Swiss residents.

What are the main restrictions on using Swiss bank crypto services?

The main restrictions involve strict KYC and AML compliance. You must verify your identity and provide proof of source of funds. Anonymous transactions are not allowed. Additionally, banks only support regulated tokens, excluding highly speculative assets. Minimum deposit requirements can also be a barrier for smaller investors.

Is my cryptocurrency insured if I store it in a Swiss bank?

Many Swiss banks offer insurance coverage for cyber incidents and theft, but the extent varies. Check the specific terms of your custody agreement. Some banks carry third-party insurance policies that cover a portion of the asset value. However, market volatility losses are not covered. Always read the fine print regarding exclusions and limits.

Which Swiss banks offer staking services?

Several major players offer staking, including Bitcoin Suisse, Sygnum Bank, and Amina Bank. Bitcoin Suisse supports staking for ETH, SOL, ADA, DOT, NEAR, and XTZ. Sygnum and Amina have recently expanded to include newer tokens like SUI. Staking allows you to earn yield on your assets while they are held in custody.

How does Swiss crypto regulation compare to the US?

Switzerland has a more mature and technology-neutral regulatory framework. They applied existing financial laws to crypto years ago, creating clarity for banks. The US has been slower, with regulators issuing guidance in 2025 to emphasize safety and soundness. This gives Swiss banks a competitive advantage in offering comprehensive, compliant services.

There are 13 Comments

Matthew Malone

Another article praising the Swiss banking system while our own regulators are still playing catch-up. It is absolutely pathetic that we have to look across the ocean for basic financial innovation. The US government creates red tape so thick you can't cut it with a knife, forcing capital to flee to Zurich and Singapore. Meanwhile, American banks are too scared to touch crypto because they don't want to lose their FDIC insurance over a regulatory technicality. We need to stop relying on foreign entities to secure our digital assets. It's a national security risk waiting to happen.

verna kennedy

The reality is that Switzerland has had decades to refine its legal framework while the US was busy fighting culture wars. FINMA provided clarity years ago. If you want safety and soundness, you go where the rules are clear. Stop complaining and start adapting to global standards instead of trying to ban what you do not understand.

Erik Kirana

It is quite amusing how people here treat 'regulatory clarity' as a virtue when it often just means legalized gambling for the elite. The average person cannot afford the €100k minimums mentioned in the text. This is not about security; it is about creating an exclusive club for the wealthy who can navigate these complex KYC hurdles. The rest of us are left with unregulated exchanges that could vanish tomorrow. Truly inspiring for the little guy.

Madhu Menon

I think we must consider the philosophical implication of trust in institutions vs code. The Swiss model attempts to bridge this gap by wrapping code in institutional armor. But does this not defeat the purpose of decentralization? Perhaps the true freedom lies in self-custody, even if it requires greater personal responsibility. 🤔

Yogendra Dwivedi

This is a very detailed breakdown of the current landscape. I am curious about the practical implications for someone like me living in India. With the strict RBI guidelines and the recent tax changes on crypto gains, does using a Swiss bank actually help with compliance or does it create more headaches with reporting? I wonder if the KYC requirements would be significantly harder for non-residents compared to local users. It seems like a robust system but accessibility remains a huge question mark for emerging markets.

Narendra Kulkarni

hii everyone i think this is really good info. i was worried about keeping my coins on exchanges after all the hacks last year. seeing that swiss banks use multi-sig and cold storage makes me feel much better. maybe i should try opening an account with aminabank since they seem more friendly to regular people than sygnum. thanks for sharing this!

JEVON HALL

Hey folks! Just wanted to drop some knowledge here 😊 The multi-sig setup mentioned is crucial. Most retail investors don't realize that 'custody' isn't just one key. Banks use HSMs (Hardware Security Modules) which are physically secured. It's basically a vault inside a vault. Also, check out the staking rewards on Bitcoin Suisse, they are pretty competitive right now 🚀 Don't sleep on the SUI token integration either, huge potential there!

Caralee Robertson

i agree with jevon hall above. the security aspect is what sells me. i've been burned before by leaving keys on a centralized exchange that went under. knowing that there is insurance coverage for cyber incidents gives me peace of mind. although i did notice typos in the terms of service once so read carefully lol. but overall this seems like the safest bet for long term holding.

Greg Lewis

you guys are missing the point entirely. it's not about the tech it's about the control. these banks are just gatekeepers pretending to be innovators. they want your data they want your identity and then they charge you fees to sit on your money. why do we need them at all when we have lightning network and self custody wallets? it's a scam wrapped in a suit.

Dr Lynea LaVoy

While self-custody is ideal for those with high technical literacy, it is not feasible for institutional clients or those managing large estates. The role of these banks is to provide a compliant bridge for traditional capital entering the space. Without this infrastructure, crypto remains a niche asset class rather than a mainstream financial instrument. Safety and accessibility often require professional management.

Kelly Tenney

I really appreciate the focus on security here. As someone who helps families plan their financial futures, I see so many people losing everything due to lack of proper safeguards. These Swiss banks offer a structured approach that protects against both external theft and internal errors. It is empowering to see options that prioritize safety without sacrificing the benefits of digital assets. Let's keep supporting systems that protect our wealth!

dan kaffeman

Only the elite will ever benefit from this. The rest of you are being sold a dream of 'security' while your purchasing power evaporates. These banks are just another layer of bureaucracy designed to extract value from you. They call it 'compliance' but it really just means 'obedience'. Wake up.

aaliyah zahid

Sarcasm aside, the integration of stablecoins for payroll mentioned in the article is actually fascinating. I work with a few startups in Toronto and they are constantly looking for ways to optimize cross-border payments. If Amina Bank's startup package is as seamless as described, it could solve a lot of friction for international teams. Though I doubt many Canadian companies are ready to jump on board yet.

Write a comment

Your email address will not be published. Required fields are marked *