央行数字货币: What They Are, How They Work, and Why They Matter

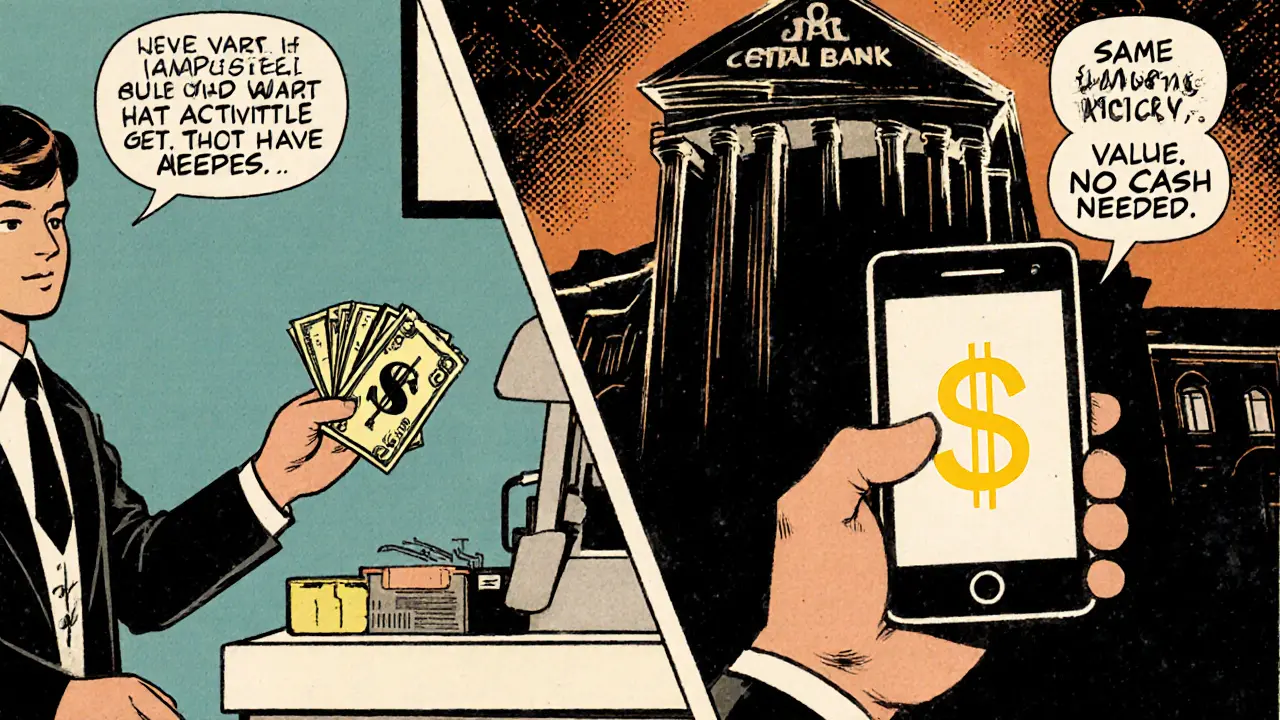

When you hear 央行数字货币, a digital form of a country’s official currency issued and controlled by its central bank. Also known as central bank digital currency, it’s not Bitcoin. It’s not Ethereum. It’s the same dollar, yuan, or euro you hold in your wallet—but in digital form, tracked by the government. Unlike crypto, which runs on decentralized networks, 央行数字货币 lives on systems the central bank owns and manages. That means no volatility, no mining, no anonymous wallets. Just state-backed money you can use in apps, ATMs, or peer-to-peer transfers.

Why are over 130 countries exploring this? Because cash is fading. In China, over 260 million people already use the digital yuan. Sweden’s e-krona tests let people pay for buses and groceries without cards. Even the U.S. Federal Reserve is researching it—not because they want to kill cash, but because they fear losing control over money if private companies like PayPal or Meta push their own digital currencies. 央行数字货币 gives governments visibility into transactions, helps stop tax evasion, and speeds up welfare payments. But it also raises real questions: Can the state freeze your money? Can they track every coffee you buy? These aren’t sci-fi fears—they’re live policy debates.

What you’ll find here are clear, no-hype breakdowns of how 央行数字货币 fits into the bigger picture of money, regulation, and blockchain. Some posts look at how national digital currencies affect crypto exchanges like WhiteBIT or Bitnomial. Others show how regulatory uncertainty around digital assets—like the ban on crypto mining in Kazakhstan or Bolivia’s trading penalties—connects to central bank decisions. You’ll see how institutions react to these shifts, why some tokens like WACME or EQX exist in this space, and how tools like blockchain node sync or validator slashing relate to the infrastructure behind digital money. This isn’t theory. It’s what’s happening now.