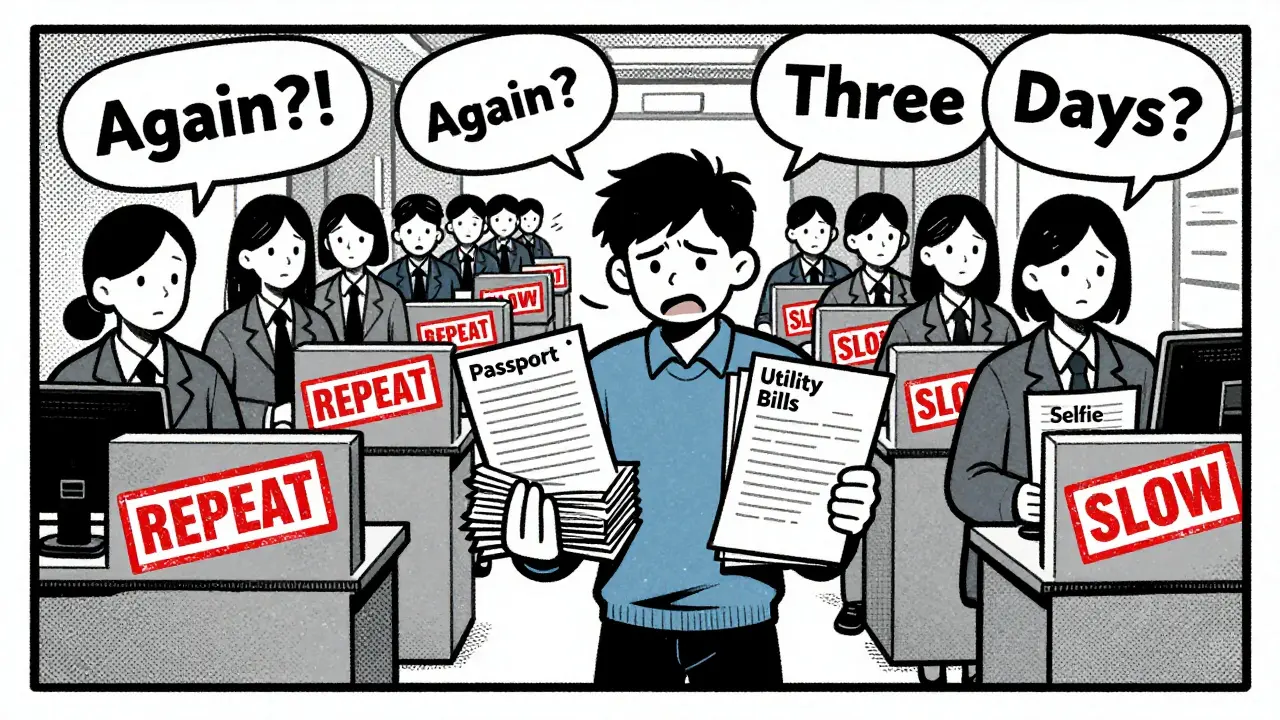

Imagine opening a new bank account. You upload your passport, take a selfie, and wait three days. Then you want to trade crypto. You do it again. Next, you need a loan. Surprise-you’re doing it all over again. This repetitive friction is exactly why KYC Verification with Blockchain is a decentralized approach to identity verification that allows users to verify their identity once and share proof across multiple institutions without revealing raw personal data gaining serious traction in 2026.

Traditional Know Your Customer (KYC) processes are broken. They are slow, expensive, and insecure. Financial institutions spend billions annually on redundant checks. Meanwhile, customers hate handing over sensitive documents repeatedly. Blockchain technology offers a fix by turning identity into a secure, reusable digital asset. But how does it actually work under the hood? And is it really safer than the old way?

The Problem with Traditional Identity Checks

Let’s look at why we even need this change. In the current system, every financial service provider operates in a silo. Bank A has no idea if Bank B already verified your identity. So when you sign up with Bank C, they treat you like a stranger. They ask for the same driver’s license, utility bills, and proof of address. You submit them again. They check them again. It’s inefficient and costly.

This redundancy creates two major issues:

- High Costs: Global banks spend roughly $5 billion to $10 billion annually just on KYC compliance. That money doesn’t come from thin air-it comes from higher fees and lower interest rates for you.

- Data Breach Risks: When thousands of companies store your raw ID data in centralized servers, you create hundreds of targets for hackers. One breach means your entire history is exposed.

A 2023 Statista survey highlighted that 88% of US adults worry about data privacy when interacting digitally. These concerns aren’t going away; they’re growing. Users demand control over their information. Traditional systems simply can’t deliver that level of security or convenience anymore.

How Blockchain KYC Actually Works

So, what changes when we move to blockchain? The core idea is simple: verify once, reuse everywhere. But the execution relies on some clever cryptography. Here is the step-by-step process of how a blockchain-based KYC system functions in practice.

- Initial Verification: You go to a trusted identity provider (like a government agency or a certified fintech). You upload your documents. They verify your identity using standard methods.

- Digital Credential Issuance: Once verified, the provider issues a digital credential. This isn’t just a PDF copy of your passport. It’s an encrypted token signed cryptographically.

- Hash Generation: The system generates a unique hash-a digital fingerprint-of your verified data. Think of a hash like a wax seal on a letter. If anyone alters the contents of the letter, the seal breaks. Similarly, if any data changes, the hash changes completely.

- On-Chain Storage: Only the hash is stored on the blockchain ledger. Your actual name, address, and photo stay off-chain, usually in your private wallet or a secure server controlled by you.

- Selective Disclosure: When you join a new service, you don’t send them your documents. You send a cryptographic proof that says, “I am over 18” or “This ID matches the hash on the blockchain.” The service checks the blockchain, sees the valid hash, and grants access.

This method ensures that the new institution never touches your raw data. They only see the verification result. It’s privacy-preserving by design.

Key Technologies Powering the System

You might wonder which tools make this possible. It’s not magic; it’s specific tech stacks working together. Let’s break down the essential components.

| Technology | Function | Why It Matters |

|---|---|---|

| Hyperledger Fabric | Permissioned Ledger Platform | Allows private networks where only authorized banks and regulators participate. Ensures confidentiality while maintaining transparency among peers. |

| Smart Contracts | Automated Logic Execution | Code that automatically checks if KYC criteria are met. No human intervention needed. Reduces error rates and speeds up onboarding to minutes. |

| IPFS (InterPlanetary File System) | Decentralized Storage | Stores heavy files like scanned IDs off-chain securely. Prevents blockchain bloat while keeping data accessible via content addresses. |

| Zero-Knowledge Proofs | Privacy-Preserving Verification | Proves a statement is true (e.g., age > 18) without revealing the underlying data (birth date). Critical for GDPR compliance. |

For example, researchers like Hanbar et al. have developed optimized e-KYC solutions using anonymous AES Key-Sharing protocols. These allow banks to share KYC info securely without exposing who is sharing what with whom. This double-blind approach adds another layer of anonymity for enterprise clients.

Benefits for Users and Businesses

Why should you care about this shift? The benefits are tangible for both everyday users and the companies serving them.

For Users:

- Speed: Onboarding times drop from days to minutes. You open accounts instantly.

- Control: You hold the keys to your identity. You decide who sees what and revoke access anytime.

- Security: Since raw data isn’t stored in one place, there’s no single point of failure. Hackers can’t steal your entire life history from one database.

For Businesses:

- Cost Reduction: Shared verification means lower operational costs. Banks stop paying for duplicate checks.

- Fraud Prevention: Immutable records mean fake IDs are harder to pass. If a document was flagged as fraudulent once, the whole network knows.

- Regulatory Compliance: Automated audit trails make reporting to regulators easier. Smart contracts log every access request, creating a perfect paper trail.

Financial institutions report significant reductions in customer friction. When a user doesn’t have to re-upload documents, they are more likely to complete the signup process. This directly boosts conversion rates for fintech apps.

Challenges and Limitations

It’s not all smooth sailing. Blockchain KYC faces real-world hurdles that prevent mass adoption overnight.

Scalability Issues: Blockchains can be slow. Processing thousands of transactions per second requires robust infrastructure. While platforms like Hyperledger Fabric handle high throughput better than public chains like Ethereum, scaling remains a technical challenge during peak loads.

Regulatory Fragmentation: Laws vary wildly by country. The EU has GDPR, which emphasizes data minimization. The US has sector-specific rules. China has its own strict digital ID laws. Building a global blockchain KYC system that satisfies all these conflicting regulations is incredibly complex.

The "Garbage In, Garbage Out" Risk: Blockchain secures the data, but it doesn’t verify the source. If the initial identity provider accepts a forged passport, the blockchain will permanently record that forgery as truth. Trust in the root issuer is still critical.

Interoperability: Not all blockchains talk to each other. A KYC credential issued on one permissioned network might not be recognized by another. Industry standards are still forming. Without universal protocols, we risk creating new digital silos instead of breaking old ones.

The Future of Decentralized Identity

Where is this heading in 2026 and beyond? The trend is clear: decentralized identity is becoming the norm, not the exception. Governments are exploring Central Bank Digital Currencies (CBDCs), which often integrate with self-sovereign identity frameworks. This means your national ID might soon live on a blockchain-compatible wallet.

We are seeing increased collaboration between competitors. Major banks that once guarded their data jealously are now joining consortiums to share KYC data securely. This shift is driven by necessity-compliance costs are too high to ignore.

Future developments will likely focus on:

- Cross-Border Standards: International bodies working on unified KYC protocols to streamline global finance.

- AI Integration: Using artificial intelligence to detect anomalies in identity submissions before they hit the blockchain.

- User-Friendly Wallets: Making identity management as easy as sending an email. Most users won’t understand hashes or private keys; they just want a button that says "Verify."

As regulatory pressure mounts and consumer expectations rise, blockchain KYC will transition from a niche experiment to a foundational infrastructure layer for the internet economy.

Is blockchain KYC compliant with GDPR?

Yes, if implemented correctly. GDPR requires data minimization and the right to be forgotten. Blockchain KYC helps by storing only hashes on-chain, not raw data. However, the immutability of blockchain conflicts with the "right to erasure." Solutions involve storing data off-chain and deleting it upon request, while leaving the empty hash on-chain as a tombstone marker. Legal teams must carefully design these workflows to ensure compliance.

What happens if I lose my private key?

Losing your private key can mean losing access to your verified identity. Unlike a password reset at a bank, there is no central authority to help you recover a lost key in a truly decentralized system. To mitigate this, many modern systems use social recovery mechanisms or multi-sig wallets where trusted contacts can help restore access. Always back up your seed phrase securely.

Can hackers alter data on the blockchain?

No. The cryptographic nature of blockchain makes it computationally infeasible to alter past records without consensus from the majority of the network. If someone tries to change data, the hash will mismatch, and the network will reject the transaction. This immutability is the core security feature protecting against fraud.

Which industries are adopting blockchain KYC first?

The financial sector leads the way, including banking, insurance, and cryptocurrency exchanges. These industries face the highest compliance costs and fraud risks. Healthcare and supply chain logistics are also exploring blockchain KYC for patient privacy and vendor verification, respectively.

Is blockchain KYC faster than traditional methods?

Significantly. Traditional manual reviews can take days or weeks. Blockchain KYC with smart contracts automates the verification logic. Once the initial setup is done, subsequent verifications happen in seconds. Even the first-time setup is streamlined because shared data reduces the amount of new documentation needed.